Affiliate tax

Our network is closely monitoring the latest information on several proposed "Nexus Tax" laws in multiple states (also called the Advertising Tax / Affiliate Tax / Amazon Tax). While some of these bills were defeated, several more are under consideration that will impact the affiliate marketing industry. These taxes could directly impact your business and your source of income.

Why does this matter?

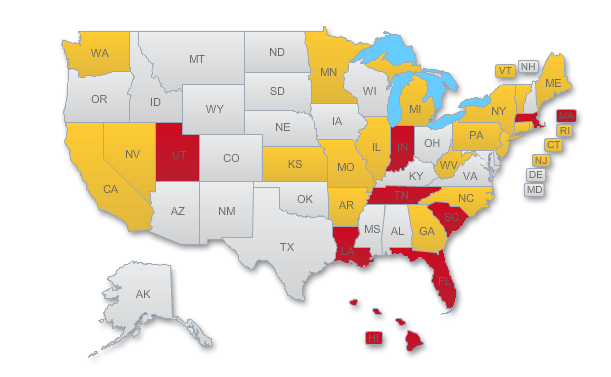

In most cases these bills require merchants to collect and remit sales tax from residents of those states because of working with affiliates in that state. As a result, some merchants may choose to end their relationships with resident affiliates to avoid this expense. For specific information on how this tax will impact your business, please contact your tax accountant.- The YELLOW states below to review the state’s respective law/statute.

- GREEN states indicate a bill, or bills that were ruled invalid through the court process.

- RED states indicate a bill that is introduced and being considered by state legislature.